1. The Shift Toward Smarter Banking Apps

A few years ago, people still walked into bank branches for simple things like transfers, card settings, or checking account statements. That behavior changed fast. Now users expect everything inside one mobile app — instant payments, budgeting tools, spending alerts, virtual cards, even currency exchange.

That shift is exactly why Banking App Development has become one of the fastest-growing areas in fintech.

Apps like Revolut changed what users expect from finance platforms. People no longer compare banking apps with traditional banks. They compare them with the speed of Uber, the simplicity of Spotify, and the experience of modern consumer apps. If a payment takes too long or the interface feels outdated, users notice immediately.

And honestly, this is where many traditional banking systems struggle. Most older banking platforms were never designed for real-time mobile experiences. Startups moved faster because they built mobile-first systems from day one.

2. What Makes a Revolut-Style App Feel Modern?

Most older banking apps still behave like web portals squeezed into a phone screen. Open the app, wait for pages to load, search through menus, maybe refresh twice because the balance didn’t update properly. Users got tired of that experience.

Revolut-style apps took a completely different route.

Everything feels immediate. Spend money? Notification arrives instantly. Need a virtual card for an online purchase? Generate one in seconds. Traveling abroad? Currency exchange happens inside the same app without calling the bank first.

That speed changed user expectations around Banking App Features.

A modern Digital Banking App usually combines multiple finance tools into one experience instead of separating everything across different products. Users can track expenses, manage cards, split bills, monitor subscriptions, and send payments from a single dashboard.

Some features people now expect almost by default:

- Instant transaction updates

- Virtual debit cards

- Smart budgeting insights

- Multi-currency support

- Card freeze/unfreeze controls

- Expense tracking

- Real-time payment alerts

But the real difference is usability. The best finance apps don’t feel “bank-like” anymore. They feel lightweight, fast, and easy to navigate. Even complex actions are reduced to a few taps.

That changes how teams approach Banking App Development. Building secure infrastructure is still critical, obviously. But now product design matters just as much. A confusing onboarding flow or slow payment screen can push users away surprisingly fast.

And this shift is happening everywhere — especially among startups building niche fintech products for travelers, freelancers, remote workers, and younger digital-first users.

Traditional banking systems move slowly. Fintech startups usually can’t afford to.

That’s one reason low-code tools started becoming part of modern Fintech App Development workflows.

3. Why FlutterFlow Started Showing Up in Fintech

Most startups don’t fail because of ideas. They run out of time.

That pressure pushed many teams toward the FlutterFlow Banking App approach. Instead of spending months building basic flows manually, founders can launch an MVP earlier and see what users actually want.

And fintech apps change constantly after launch anyway.

A modern FlutterFlow Banking App can handle things like payments, authentication, transaction history, and real-time dashboards without a massive development cycle in the beginning.

The appeal is simple: faster testing.

Need to improve onboarding? Add a budgeting screen? Change the payment flow? Teams can move quicker without rebuilding the whole app every few weeks.

For startups working on Banking App Development, that flexibility matters more than people realize.

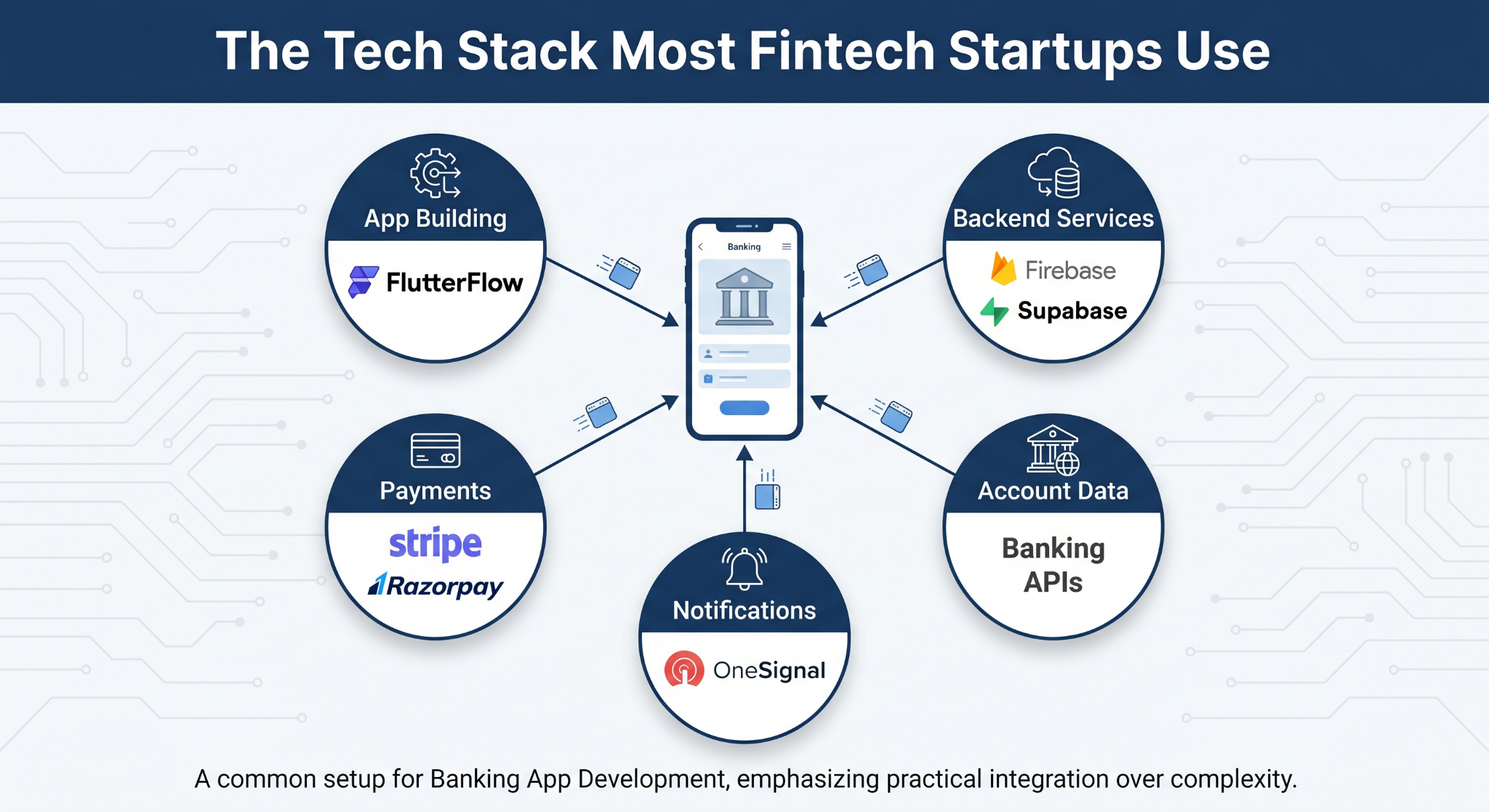

4. The Tech Stack Most Fintech Startups Use

Banking apps aren’t just frontend screens connected to a database. Payments, notifications, authentication, and financial data all have to sync properly — and fast.

That’s why many startups keep the stack practical instead of overcomplicated.

A common setup for Banking App Development now looks something like this:

- FlutterFlow for app building

- Firebase or Supabase for backend services

- Stripe or Razorpay for payments

- Banking APIs for account data

- OneSignal for notifications

For teams building a FlutterFlow Banking App, the advantage is usually speed. The app can launch earlier, features can change faster, and smaller teams can handle updates without massive engineering overhead.

And honestly, most startups care about that more than having an overly complex architecture on day one.

5. Cost and Timeline of Banking App Development

The timeline depends heavily on what you’re building.

A basic MVP with core payments, onboarding, and transaction tracking can launch in a few months. A full-scale fintech platform with advanced compliance systems, analytics, and multi-currency infrastructure takes much longer.

That’s why many startups begin small.

In most cases, Banking App Development costs increase because of:

- Security requirements

- Payment integrations

- Compliance systems

- Custom backend logic

- Scaling infrastructure

This is also where low-code development changes things a bit. A FlutterFlow Banking App can reduce early development time because teams spend less effort building standard app flows from scratch.

Instead of waiting a year to validate an idea, startups can launch faster, collect feedback, and improve the product gradually.

That approach is becoming pretty common in fintech now.

6. Launching a Fintech App Is Easier Than It Was a Few Years Ago

A few years back, building a finance app usually meant hiring a large team before the first screen even went live. For startups, that was rough. Development costs piled up early, and product testing happened late.

Things changed pretty quickly.

Platforms like Arixlabs (previously FlutterFlowDevs) help startups skip a lot of the slow setup work by starting with pre-built fintech systems instead of empty projects.

For businesses entering Banking App Development, that can save months of early effort. Teams can focus more on product ideas, onboarding experience, and customer feedback instead of rebuilding common app flows repeatedly.

The same thing applies to a Digital Banking App. Most successful fintech products don’t launch perfectly on day one anyway. They improve after real users start interacting with the app.

That’s why faster launches matter now more than oversized first versions.

7. Conclusion

Finance apps are changing faster than most traditional banking systems can keep up with. Users expect instant payments, smart insights, and simple experiences without the friction older apps usually create.

That shift is pushing startups toward faster product development cycles, leaner teams, and flexible low-code workflows. And honestly, that trend probably won’t slow down anytime soon.

FAQs

What is a digital banking app?

A Digital Banking App lets users manage financial activities like payments, transfers, budgeting, and card controls directly from a mobile device.

Does FlutterFlow support fintech integrations?

Yes. A FlutterFlow Banking App can connect with payment gateways, banking APIs, authentication systems, and backend services.

Can I launch a banking MVP first?

Most startups do exactly that. Launching a smaller MVP helps teams test features early before scaling the platform further.

Which APIs are commonly used in banking apps?

Payment APIs, banking data APIs, authentication services, and notification systems are commonly used in fintech platforms.

%20(1).jpg)

View more blogs

.png)

.png)

.png)

.png)

.png)

.jpg)

.png)

Ready to develop your own product? Get in touch today!

Get in Touch